When Jensen Huang announced Nvidia’s $1 trillion AI chip revenue forecast, the stock promptly fell 0.9%—a perfect encapsulation of where we are in the AI infrastructure cycle. That disconnect between headline-grabbing numbers and market yawn tells you everything about how Wall Street now views these astronomical projections. The trillion-dollar figure sounds earth-shattering until you realize it’s just an extension of existing trends through 2027, not evidence of accelerated growth.

The Agentic AI Economy Drives Infrastructure Demand

The confidence behind that trillion-dollar bet hinges on what Nvidia calls the “token-driven AI economy“—where running deployed AI models becomes more economically important than training them. Anthropic’s Claude Code serves as exhibit A: Huang notes that every software engineer at Nvidia now uses AI agents for coding assistance. When AI systems need to continuously reason and interact rather than just complete training runs, the infrastructure math changes completely. Your future AI assistant won’t just need processing power—it’ll need sustained inference performance that traditional GPU setups struggle to deliver efficiently.

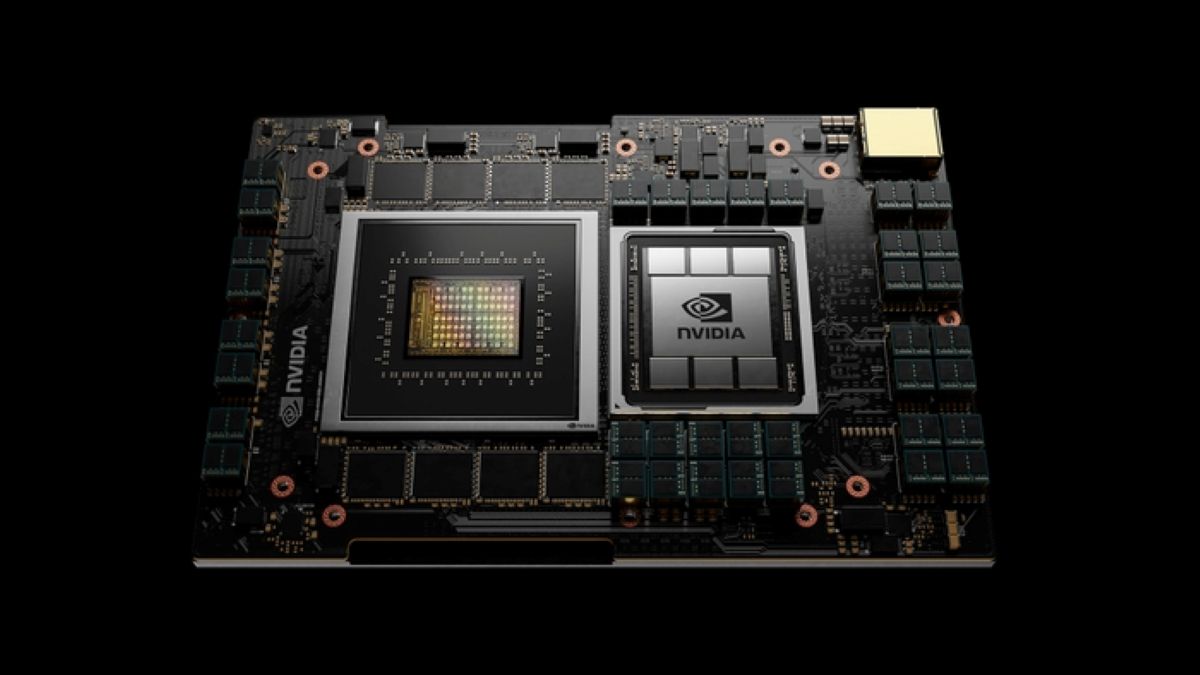

From GPU Cards to AI Supercomputers

Nvidia’s Vera Rubin platform represents a fundamental shift from selling individual GPU cards to “productizing the rack”—designing complete, validated systems that function as unified AI supercomputers. The flagship NVL72 combines 72 GPUs, 36 CPUs, and Nvidia’s networking into a single coherent system with 3.6 TB/s of GPU-to-GPU bandwidth. It’s like Apple’s approach to hardware integration, but for data centers. This matters because inference workloads demand different optimization than training—more about sustained throughput and memory efficiency than raw computational bursts.

Hyperscaler Dependency Remains the Hidden Risk

Despite Nvidia’s efforts to diversify, hyperscalers—Amazon Web Services, Google Cloud, Microsoft Azure, and Meta—still represent 60% of the projected trillion-dollar opportunity. That concentration would make most CFOs nervous, especially when you’re betting on sustained multi-billion-dollar annual commitments from essentially four customers. The market’s lukewarm response suggests investors recognize this dependency hasn’t materially improved, even as the addressable market expands.