Those blue Bed Bath & Beyond coupons cluttering your junk drawer just became retail artifacts, joining Circuit City receipts in America’s shopping graveyard. The US retail landscape is experiencing a slow-motion collapse that would make a Windows Vista crash seem lightning-fast by comparison.

While everyone blames Amazon for this carnage, the real story involves private equity vultures, pandemic aftershocks, and leadership teams with all the adaptability of a Nokia brick phone. These retailers are scrambling to reinvent themselves in a market that shows no mercy to the unprepared. Some might surprise you – others are exactly where you’d expect them to be.

17. Sears: The Retail Walking Dead

Sears became retail’s walking dead, operating fewer than 20 stores nationwide after once being America’s largest retailer with 3,500+ locations. This 99.5% reduction makes other retail failures seem minor by comparison, representing one of the greatest destructions of retail value in business history.

From selling everything from houses to hammers through its revolutionary catalog system, Sears failed to adapt to e-commerce competition despite literally inventing the model Amazon perfected. The remaining stores operate in the manner of retail museums with outdated fixtures, sparse inventory, and employees who seem as surprised as customers that they’re still open for business.

16. Foot Locker: Losing Its Sneaker Game

Stuck amid brand partners and direct sales? Foot Locker feels the crushing pain of Nike’s direct-to-consumer pivot with all the intensity of a sneakerhead getting ghosted by their favorite brand. The athletic retailer plans to close 400 underperforming mall locations by 2026 while opening 300 new concept stores focused on community experiences rather than traditional retail approaches.

When brands such as Nike and Adidas prioritize their own channels over wholesale partnerships, sneaker retailers face an existential crisis deeper than choosing among Jordan 1s and Dunks. Foot Locker must execute a tricky transition from sneaker seller to lifestyle destination, competing against brands that control their own destiny.

15. Neiman Marcus: Luxury in Survival Mode

Luxury doesn’t guarantee immunity from bankruptcy, as Neiman Marcus learned while grappling with $1.1 billion in remaining debt after emerging from 2020 bankruptcy. The upscale department store focuses on fewer, better stores rather than widespread expansion, acknowledging that luxury retail requires a different playbook than mass market strategies.

The company faces competition from brands’ direct channels and online luxury platforms while wealthy shoppers increasingly value experiences over goods. Neiman’s $200 million store renovation investment attempts to redefine luxury retail for an era where exclusivity gets defined by limited drops and digital communities rather than traditional high prices alone.

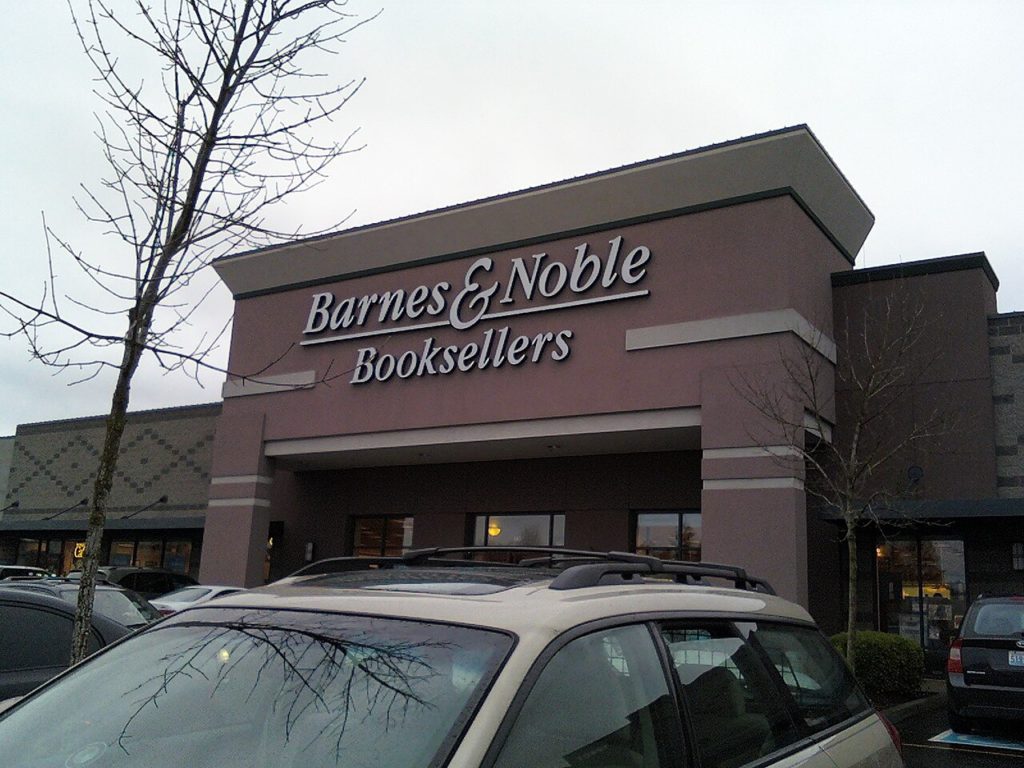

14. Barnes & Noble: Plot Twist Worth Reading

If you’re betting against bookstores in the digital age, Barnes & Noble might surprise you with its unlikely comeback story. After years of decline and 2019 acquisition by Elliott Advisors, the bookstore chain showed surprising signs of life – opening 16 new stores in 2022 and planning 30 more in 2023.

The turnaround strategy under CEO James Daunt involves giving local stores more autonomy and treating books comparable to fashion merchandise requiring regular refreshing. This approach acknowledges what Amazon can’t replicate: the serendipity of discovering books you weren’t looking for, proving that sometimes physical retail can adapt rather than surrender.

13. Macy’s: Shrinking to Survive

Department store relevance just got 25% smaller with Macy’s closing 125 locations by 2023 as part of its “Polaris” transformation strategy. Despite $24.4 billion in annual revenue, the stock hovers near pandemic lows, resembling a once-popular app battling for relevance.

The retailer responded by investing in digital platforms, developing smaller-format stores, and expanding its Backstage off-price concept to compete with TJ Maxx. With 500+ remaining locations and careful navigation required, Macy’s attempts to demonstrate that department stores retain relevance in an age when Amazon delivers everything quicker than most people change their minds.

12. Kmart: The Retail Zombie

Hunting for retail nostalgia feels about as likely as spotting a functional payphone when you’re looking for an open Kmart. Once boasting 2,400 locations, Kmart now operates just three stores nationwide, a 99.9% reduction that makes even the Titanic disaster seem manageable by comparison.

After the 2005 Sears merger, Kmart suffered from chronic underinvestment and stores that time forgot more rapidly than MySpace profiles vanished from the internet. The remaining stores in Florida, Long Island, and New Jersey exist as retail curiosities rather than actual businesses, resembling museums nobody asked for.

11. Party City: The Party’s Definitely Over

Flat attendance at celebrations can hurt any party business, but Party City’s bankruptcy in January 2023 proved that $1.7 billion in debt kills even the best party atmosphere. The once-dominant party supplier closed hundreds of locations, shrinking from 850 to around 750 stores nationwide with all the grace of a deflating balloon.

The company’s troubles predate pandemic party cancellations, stemming from competition with dollar stores, Amazon, and big-box retailers offering comparable products without requiring a special trip. Helium shortages literally deflated one of its key profit centers, proving that sometimes the universe has a sense of irony about struggling businesses.

10. Express: Fashion Emergency Alert

Express is sending SOS signals from abandoned mall corridors with all the desperation of a Nokia trying to compete with smartphones. The fashion retailer’s stock collapsed 97% over five years, trading below $1 and risking NYSE delisting more swiftly than a TikTok trend dies.

The brand that once defined accessible workplace style now wrestles with remote work reality, athleisure dominance, and fast-fashion competition that moves at Instagram speed. Express’s attempt to launch UpWest lifestyle brand feels comparable to throwing multiple strategies against the wall hoping something sticks, which rarely works in fashion or life.

9. Walgreens: Prescription for Retreat

Inventory shortages at competitors can boost sales, but Walgreens faces the opposite problem – it’s retreating from entire markets while competitors gain ground. The pharmacy giant shuttered 150 U.S. locations plus 300 UK stores, signaling trouble despite its massive 8,500+ U.S. footprint that once seemed as permanent as Google’s dominance.

Closures stem from rising theft, staffing challenges, and shifting consumer habits that favor convenience over proximity. Walgreens’ expensive healthcare clinic bet through VillageMD hasn’t delivered expected returns, forcing a $5.8 billion write-down that stings worse than a failed startup’s Series A rejection.

8. JCPenney: Retail’s Awkward Middle Child

Trapped amid discount and luxury retail, JCPenney knows your pain – the retailer occupies retail’s most dangerous territory where nobody wants to shop. Not upscale enough to compete with Nordstrom, not cheap enough to battle Walmart, this 121-year-old retailer emerged from 2020 bankruptcy with new owners but the same identity crisis.

The infamous 2012 reinvention under former Apple executive Ron Johnson eliminated sales and coupons, alienating customers more speedily than a mandatory Windows update clears your desktop. Today’s JCPenney attempts another comeback through Sephora partnerships, but being stuck in retail’s middle feels equivalent to being trapped in traffic while everyone else moves forward.

7. Office Depot: Running Low on Everything

Business paperwork creates demand for office supplies, but Office Depot battles when remote work eliminates that need permanently. Operating approximately 1,000 stores after peaking at 1,900+ locations, the retailer fights to justify its existence when Amazon Business delivers everything speedier and cheaper.

The 2013 OfficeMax merger failed to produce a competitor strong enough to thrive independently, leading to multiple failed acquisition attempts that feel increasingly desperate. As businesses reduce paper consumption and embrace digital workflows, Office Depot faces the challenge of convincing companies they need dedicated office supply stores in a paperless world.

6. Rite Aid: Prescription for Disaster

Competition intensifies among pharmacies daily, and Rite Aid’s vital signs flatlined when it filed Chapter 11 in October 2023. Weighed down by $3.3 billion in debt and plans to close 154 underperforming locations, the pharmacy chain resembles a patient on life support while CVS and Walgreens perform surgery to steal its customers.

While rivals expanded healthcare services and modernized operations with the efficiency of a Tesla software update, Rite Aid remained stuck in pharmacy purgatory. This marks the third-largest retail bankruptcy of 2023, which tells you everything about how brutal this year has been for brick-and-mortar stores.

5. Bed Bath & Beyond: The Final Checkout

Watching retail failure unfold in slow motion, Bed Bath & Beyond provides the perfect case study. Filing for bankruptcy in April 2023 after burning through $5.2 billion in debt more rapidly than customers burned through those infamous 20% off coupons, the home goods giant closed all 360 stores.

While Target embraced digital transformation and Amazon ate everyone’s lunch, BB&B doubled down on cluttered stores and paper coupons as if the calendar still read 1999. When Overstock bought the brand’s intellectual property for $21.5 million, it was retail’s equivalent of buying a Ferrari engine for scrap metal prices.

4. Gap Inc.: Generation Gap Crisis

Brand identity confusion reaches peak levels when Gap Inc. closes stores more swiftly than teenagers abandon mall food courts for bubble tea shops. Planning to shutter 350 Gap and Banana Republic stores by 2023’s end, the company behind multiple brands contends with identity confusion across its portfolio.

Gap drifted from classic American basics, Banana Republic lost professional wear dominance in the work-from-home era, and Old Navy faced inventory missteps that frustrated loyal customers. Only Athleta shows consistent growth, reflecting broader consumer shifts toward activewear that prioritizes comfort over corporate dress codes nobody misses.

3. Big Lots: Not So Big Anymore

If you’re seeking discount furniture treasures, Big Lots wants to be your destination but increasingly nobody’s buying what they’re selling. The stock has plummeted 90% since 2021, trading at levels not seen since dial-up internet ruled the world and flip phones were considered cutting-edge technology.

Walking through Big Lots today feels akin to visiting a clearance concept that lost its way, with half-stocked shelves and dimly lit corners lacking the treasure-hunt appeal that drives traffic to TJ Maxx. Without a compelling reason to choose Big Lots over countless alternatives, this discounter risks becoming an even bigger markdown than its own merchandise.

2. Tuesday Morning: Morning After Regret

Home goods liquidation just got more permanent with Tuesday Morning’s second bankruptcy in three years this February. Announcing closure of all 487 stores and ending a 49-year retail run with all the fanfare of a deleted Instagram story, the home goods discounter’s name became unintentionally prophetic.

Unlike TJ Maxx, which mastered the art of reliable surprise shopping experiences, Tuesday Morning stores felt equivalent to the clearance section of a store already on clearance. With $87.7 million in debt and failed financing attempts, the retailer that specialized in closeout merchandise became the ultimate closeout itself.

1. Nordstrom: Luxury Under Digital Pressure

Sandwiched across traditional luxury retail and digital disruption? Nordstrom feels your pain while closing 15 locations in 2023 including its San Francisco flagship after 35 years of operation. The upscale department store faces competition from online platforms such as Farfetch and Net-a-Porter that offer luxury shopping without the mall trip.

With stock down 30% over five years and revenue below pre-pandemic levels, Nordstrom recalibrates its approach to luxury retail in the manner of a premium brand adjusting to changing tastes. The retailer famous for customer service must now serve itself a dose of innovation to remain relevant to younger luxury shoppers who value experiences over traditional shopping.